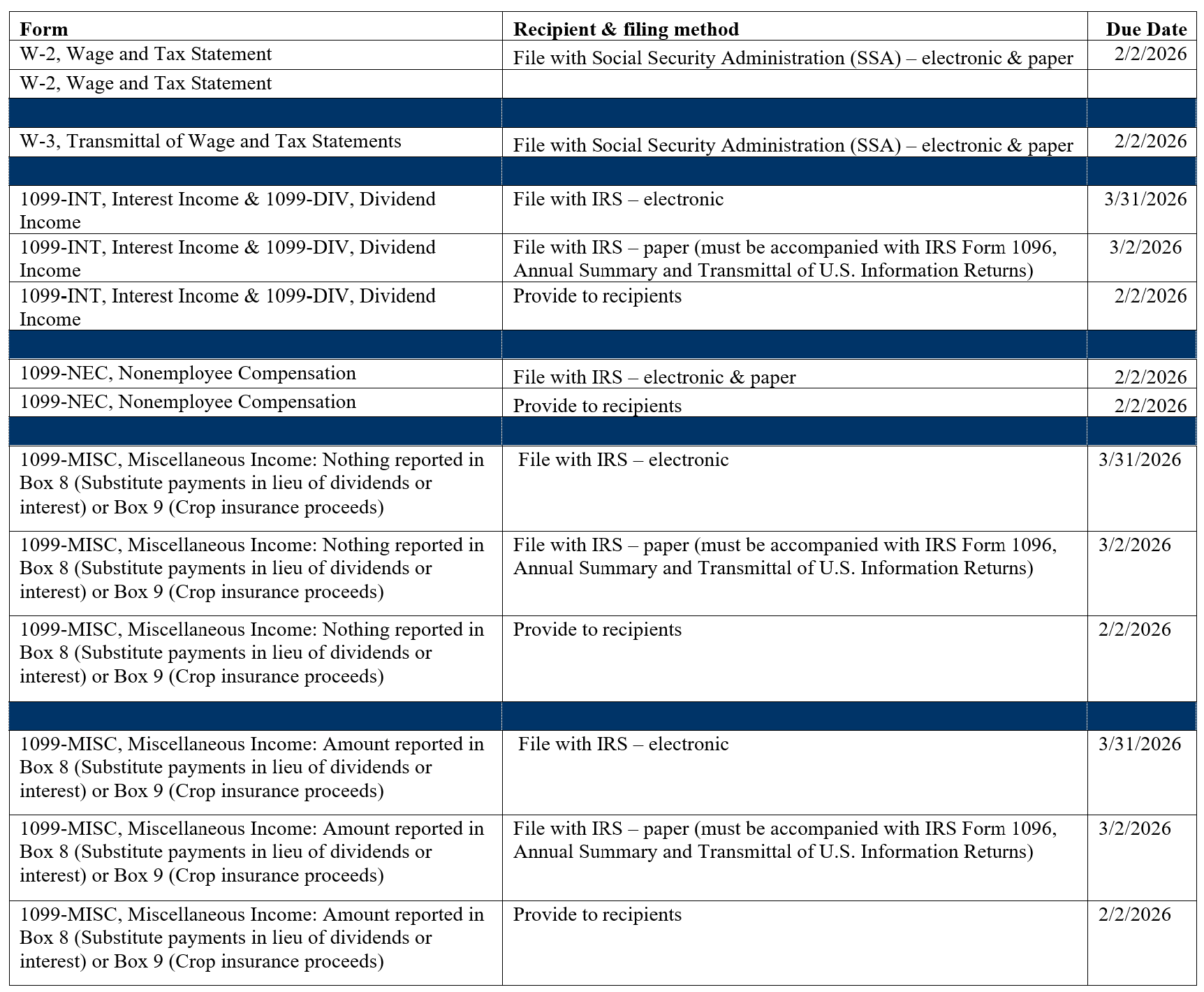

Special Issue - Tips & Overtime

Federal:

The One Big Beautiful Bill Act (OBBBA) enacted in July 2025, allows certain employees to deduct tips and overtime compensation. One area of uncertainty, affecting both employers and employees, regards 2025 payroll reporting for tips and overtime.

Under the OBBBA, from 2025 to 2028, certain employees who receive qualified:

- tips may deduct up to $25,000 of those tips, and/or

- overtime pay may deduct up to $12,500 of qualified overtime compensation ($25,000 for joint filers).

To enable employees to report their deduction, the OBBBA requires employers to provide separate accounting of the total amount of cash tips and overtime. Employers failing to comply with these reporting requirements may be subject to penalties.

Although the IRS has released a draft version of Form W-2 for 2026 reflecting OBBBA changes, the 2025 version of the form will not be updated, creating a challenge for employer reporting compliance. As a result, for tax year 2025, the IRS announced in that employers will not face penalties for failing to provide required tip and overtime accounting to employees (Notice 2025-62). This relief only applies to tax year 2025 because the IRS recognizes that employers might not have the information required to be reported.

For 2025, the IRS encourages employers to provide some accounting so employees can claim the deduction on their federal tax returns. The IRS has stated that employers may report the amounts of qualified tips and overtime to employees through secure methods, including an online portal or additional written statements provided to employees. When reporting these amounts, employers should not stop at the maximum of $25,000 (tips) or $12,500 (overtime). The full amounts of qualified tips and overtime should be reported. It is up to employees to determine the maximum deductible amount when preparing their federal income tax returns.

With little authoritative guidance and difficulty getting full information from existing systems and payroll providers, employers must do their best in providing employees with this information. Employers could, for example, provide the information by separate letter or use W-2 Box 14 (Other). For the most current guidance (updated as issued), go to: https://www.irs.gov/newsroom/one-big-beautiful-bill-provisions and click on “No tax on tips (Section 70201)” and “No tax on overtime (Section 70202).”

MA, CT, ME, RI, VT, NY: These states do not allow employees to deduct tips or overtime; thus, this reporting issue does not impact NE and NY payroll reporting.